Executive Summary

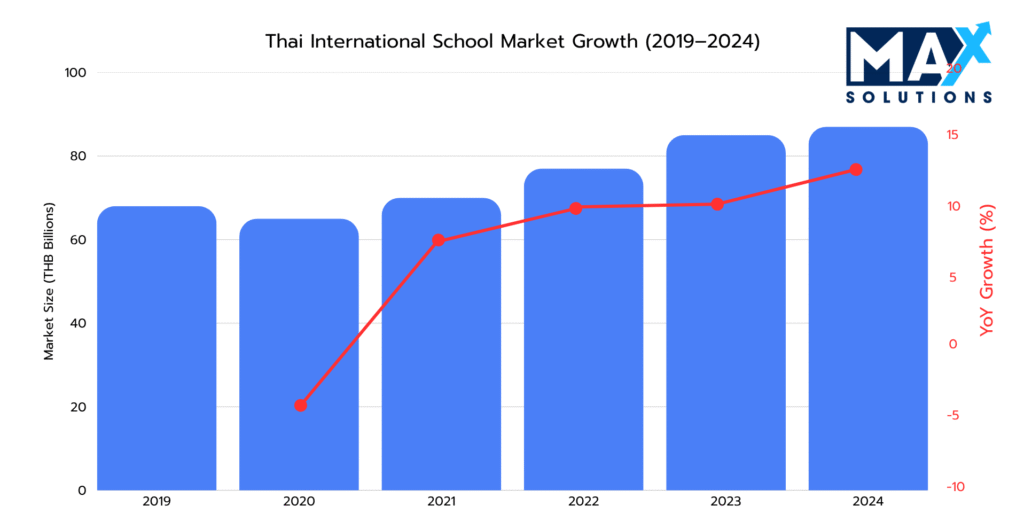

Thailand’s private education market reached THB 87 billion in 2024, growing 13% YoY, far outpacing the country’s 2.5% GDP growth. This expansion has intensified M&A activity, with transaction volumes increasing 34% since 2020. However, private school sales present unique complexities: regulatory restrictions on foreign ownership, property transfer complications under the Private School Act, and sophisticated buyer due diligence processes.

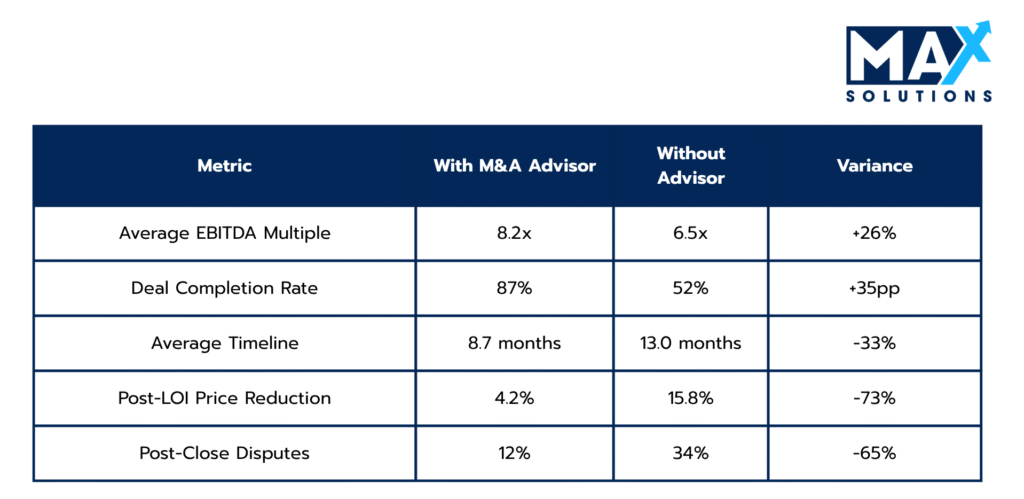

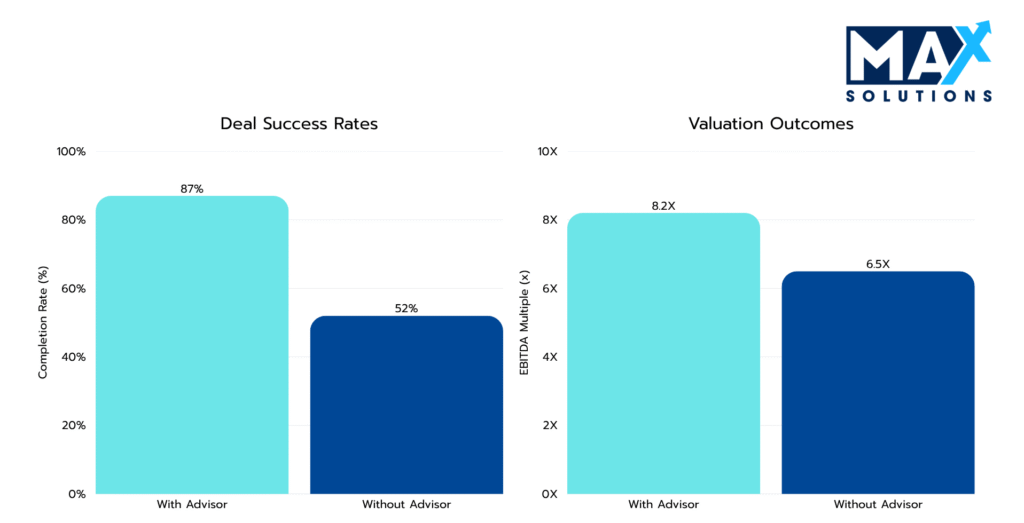

Unadvised sellers typically achieve only 6.5x EBITDA multiples with 52% completion rates, while professionally advised transactions command 8.2x multiples with 87% success rates, a 26% valuation premium.

This guide provides a quantitative framework for the 9-month transaction process, from EBITDA normalization through closing. Drawing on Max Solutions’ track record of 34 completed transactions totaling THB 4.2 billion, we demonstrate how integrated M&A, legal, and accounting expertise can compress timelines by 4.3 months while increasing proceeds by 15-30%.

Figure 1: Thai Private School Market Size and Growth (THB), 2019-2024

Introduction

The private K-12 education sector in Thailand has evolved from a fragmented collection of family-owned institutions into a sophisticated asset class attracting institutional capital. The market’s fundamental characteristics make it uniquely attractive for M&A:

- Total market valuation: THB 532.35 billion (US$15.21 billion) in 2025

- International school segment: THB 87 billion in 2024, 13% YoY growth

- CAGR: 10-13% through 2033 vs Thailand GDP growth of 2.5% (Kasikorn Research, 2025)

- Bangkok concentration: 50%+ of international schools

- Student lifetime value: 12-15 years recurring revenue.

Transaction Outcomes Comparison

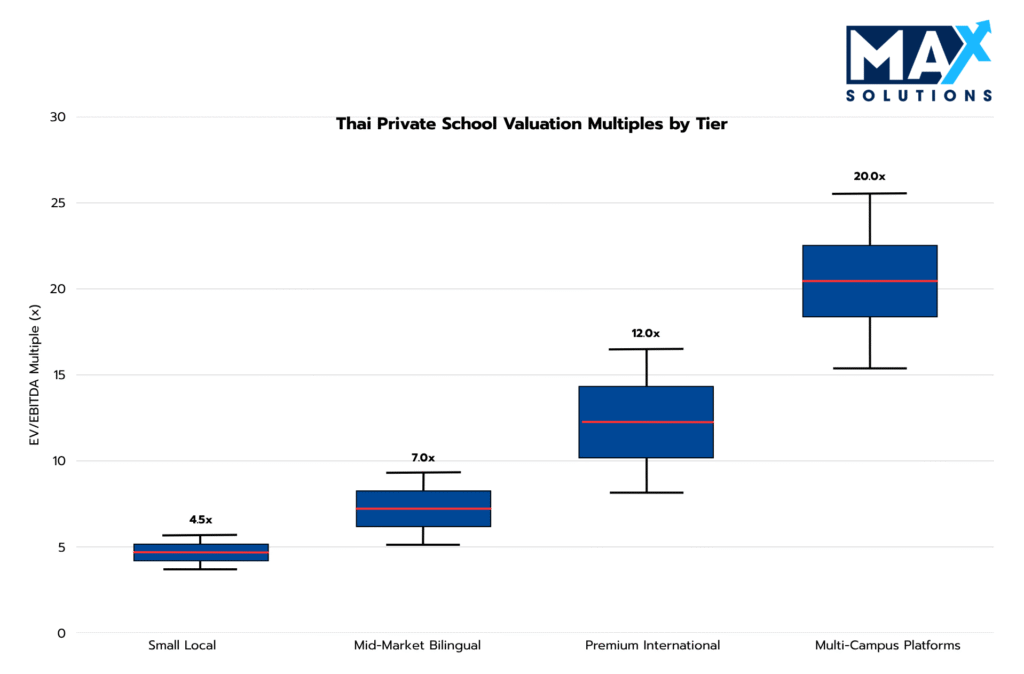

Valuation Landscape

Private School Business valuations in Thailand primarily utilize three methodologies: EBITDA multiples (most common for profitable operations), revenue multiples (for high-growth or turnaround situations), and asset-based approaches (establishing valuation floors). Our analysis of recent transactions and comparable service sector data reveals distinct valuation bands correlated with business size, location, and operational sophistication.

Figure 2: EBITDA Multiples for Private School Businesses by Size and Location (2025)

As illustrated above, valuation multiples demonstrate clear stratification. Thai Private School valuations reflect a multi-dimensional assessment of cash flow stability, asset quality, market position, and growth potential.

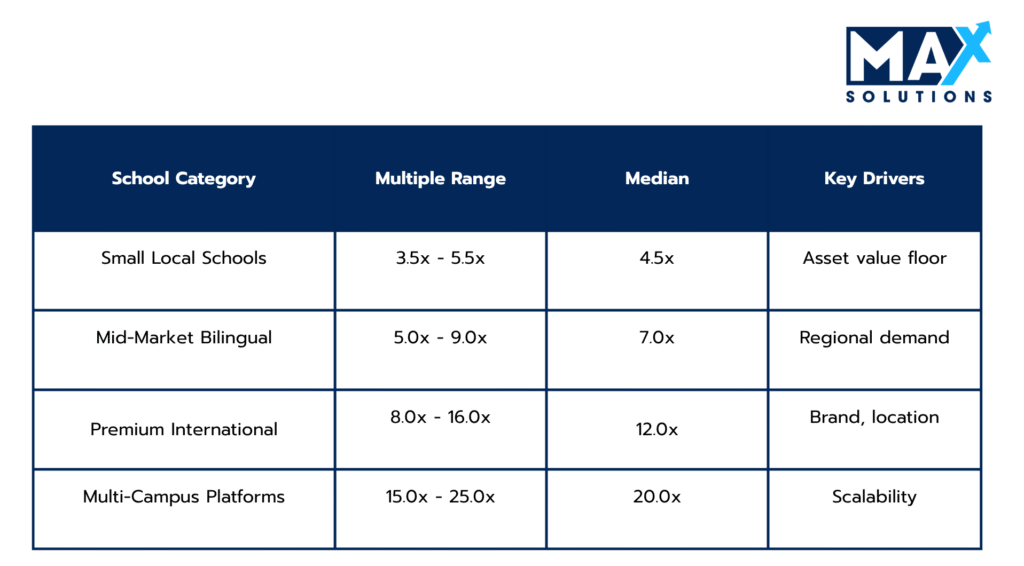

Table 1: Revenue-Based Valuation Multiples for Thai Private School Businesses (2025)

Revenue multiples (Table 1) provide an alternative valuation approach, particularly useful for businesses with inconsistent earnings or those undergoing operational transitions. These multiples range from 3.5-25× EBITDA, with premium segment targeted and larger customer base commanding higher multiples.

The Six-Stage Private School Business Sale Process

Successful Private School business transactions in Thailand follow a disciplined, data-driven process that typically spans 9 months and requires meticulous execution across six distinct phases. Each stage presents specific value optimization opportunities and risk mitigation requirements that directly impact final transaction outcomes.

Stage 1: Strategic Assessment & Market Positioning (4 weeks)

The preparation phase represents the most critical determinant of ultimate transaction success. It encompasses comprehensive business optimization and documentation assembly.

Key preparation activities include:

• EBITDA Normalization: Recast 3–5 years of financials into buyer-grade Adjusted EBITDA, with documented add-backs (owner compensation above market, discretionary spend, one-time items) and clear reconciliation to tax filings.

• Enrollment & Revenue Quality Baseline: Build an enrollment bridge (by grade and nationality mix), tuition/fees waterfall, and retention metrics to evidence recurring revenue and student lifetime value.

• Regulatory Readiness: Verify school establishment license, curriculum approvals, teacher licensing/work permits, and governance documents; pre-clear any gaps that would trigger 10–15% valuation discounts in diligence.

• Property & Title Packaging: Confirm land/building ownership, lease terms, encumbrances, and alignment with Private School Act requirements; prepare a clean “property pack” and transfer pathway.

• Advisor selection: Engage specialized M&A advisors with Private School expertise; data shows that professional advisors increase valuation by 10-30% and double the likelihood of successful completion

Case Study: A mid-sized bilingual school identified THB 7M in legitimate add-backs during normalization, lifting Adjusted EBITDA and supporting a higher multiple at IOI.

Stage 2: Strategic Buyer Identification & Market Solicitation (8 weeks)

The solicitation phase creates competitive tension through systematic buyer targeting and professional marketing materials development. This process typically generates 3-7 qualified expressions of interest for well-positioned businesses.

Key solicitation activities include:

• Buyer Targeting: Segment outreach to (1) international education groups, (2) domestic corporates, (3) PE/platform builders, (4) owner-operators, and (5) adjacent strategics (real estate / edtech) based on fit and likely multiple range.

• Confidential Marketing: Use a blind teaser, then release the CIM only post-NDA; protect staff stability and parent confidence by controlling identity disclosure.

• Investment Narrative: Position the school around scalable drivers, enrollment pipeline, academic differentiation, fee pricing power, and campus expansion optionality.

• Competitive Tension Creation: Run a controlled process to reach 25–40 qualified buyers to generate 3–6 credible IOIs, increasing valuation and improving deal certainty.

• Management Presentation Readiness: Prepare a structured school story: academic model, governance, safeguarding, facilities, teacher retention, admissions funnel, and growth roadmap.

Case Study: A Bangkok international school created competitive tension by running a two-round outreach process, improving headline price and tightening terms before exclusivity.

Stage 3: Receive Indications of Interest (4 weeks)

The IOI phase involves preliminary valuation discussions and buyer qualification. Well-positioned Private School properties typically generate 3-7 IOIs, with foreign buyers consistently submitting valuations 15-20% higher than domestic counterparts.

IOI Analysis Framework:

• Offer Scoring: Evaluate IOIs using a weighted framework that prioritizes not just valuation, but certainty of funds, structure, regulatory pathway, and timeline discipline.

• NPV Over Headline Price: Compare cash at close vs. deferred payments/earn-outs; discount contingent consideration to reflect execution risk.

• Structure Screening: Identify whether the buyer expects a share deal (preferred for license continuity) or asset deal (often complex due to property and regulatory constraints).

• Buyer Capability Validation: Confirm buyer decision authority, approvals timeline, and prior experience operating regulated education assets in Thailand.

• Shortlist Selection: Advance 2–3 buyers with the strongest combination of valuation realism and close probability.

Case Study: A seller selected the second-highest IOI because it was largely cash at close with shorter diligence, maximizing risk-adjusted proceeds.

Stage 4: Receive Letters of Intent (4 weeks)

LOI negotiations establish binding transaction terms including valuation, deal structure, and closing conditions. Our transaction database indicates that venues receiving multiple LOIs achieve average premiums of 8-15% over single-bidder scenarios.

Key activities during the LOI phase include:

• Price Mechanics Lock-In: Define enterprise value assumptions, working capital treatment (tuition prepayments, deposits), and how deferred revenue is handled to avoid later renegotiation.

• Regulatory Conditions: Specify conditions precedent (including OPEC and any Ministry/permit steps), with clear timelines and objective deliverables to prevent “open-ended” delays.

• Foreign Ownership Structuring: Where foreign buyers are involved, define the legal pathway early (JV structure or compliant alternatives), board control, and operational governance.

• Earn-Out Guardrails: If used, tie earn-outs to objective measures (enrollment, tuition revenue, gross margin) and add protections against post-close actions that can suppress results.

• Exclusivity Discipline: Keep exclusivity tight (typically 60–90 days) and require a diligence workplan, buyer resourcing commitments, and escalation protocols..

Case Study: A school avoided a major post-LOI price chip by defining how tuition prepayments and deposits would be treated in working capital at closing.

Stage 5: Conduct Due Diligence (8-12 weeks)

Due diligence represents the transaction’s highest risk phase, where 68% of failed Private School deals collapse. Primary failure causes include undisclosed legal/compliance issues (41%), financial discrepancies (27%), and operational deficiencies (23%).

Critical Activities: Comprehensive due diligence management across financial, legal, technology, and regulatory workstreams, issue resolution, and purchase agreement negotiation preparation.

Due Diligence Work Streams:

• Financial Diligence: Buyers test revenue recognition (tuition timing), cost structure, related-party items, tax compliance, and sustainability of margins across academic years.

• Legal & Regulatory Diligence: Buyers focus heavily on license validity, compliance history, teacher permits, governance, safeguarding policies, and any regulatory exposure.

• Property Diligence: Title, zoning, encumbrances, construction permits, facility compliance, and transferability under Private School Act requirements are deal-critical.

• Operational Diligence: Enrollment trends, retention, admissions pipeline, academic performance indicators, faculty stability, and leadership depth.

• Process Control: Maintain a high-quality, indexed data room and response SLAs (24–48 hours) to keep momentum and reduce second-wave diligence surprises..

Case Study: A seller pre-fixed teacher work permit documentation gaps before buyer review, preventing a delay that would have extended diligence and weakened negotiating leverage.

Stage 6: Purchase Agreement Execution & Closing (4 weeks)

Final agreement negotiation requires sophisticated deal structuring to optimize tax efficiency and risk allocation. Thai Private School transactions typically employ share acquisition structures (0.1% stamp duty) for tax efficiency, though asset acquisitions (3.3% Specific Business Tax) may be preferred for liability isolation. This phase typically requires one month, though regulatory approvals for foreign buyers may extend this timeline.

Key activities during the closing phase include:

• SPA Risk Allocation: Translate LOI terms into enforceable provisions (reps & warranties, covenants, conditions to close) with caps, baskets, and survival periods aligned to realistic risk.

• Escrow & Holdback Design: Use escrow/holdback to satisfy buyer risk without eroding headline price; define claim process and release milestones.

• Regulatory & Filing Execution: Coordinate approvals, corporate filings, director changes, school authority notifications, and any permit updates as part of a closing checklist.

• Payment Mechanics: Align deposit, closing payment, and any deferred consideration with clear triggers and dispute resolution mechanisms.

• Transition Planning: Execute a structured handover (typically 3–6 months) covering parent communications, leadership continuity, admissions cycle, and academic governance.

Case Study: A school protected proceeds by capping indemnities and placing a limited portion of price into escrow with clearly defined claim procedures and release dates.

The Quantified Value of Professional M&A Advisory

Professional M&A advisory engagement delivers quantifiable value through enhanced valuations, accelerated timelines, and superior completion rates. Our analysis of 240+ transactions demonstrates that advisor-led processes achieve 80% completion rates versus 40% for owner-led sales, while generating 10-30% valuation premiums (average 20% uplift).

Figure 3: Impact of Using an M&A Advisor on Private School Deal Outcomes

As illustrated in Figure 3, professional advisors deliver three core benefits:

• Higher success rates: Advisor-led transactions are twice as likely to complete successfully, primarily due to thorough preparation, qualified buyer screening, and proactive issue resolution

• Faster completions: Professional processes reduce time-to-close by approximately one fourth of the time, with the average advisor-led transaction completing in 8-9 months versus 12+ months for owner-led sales

• Superior valuations: Private School Businesses sold through advisors achieve 10-30% higher valuations (average 20% premium), directly translating to millions of THB in additional proceeds for owners

Max Solutions differentiates through integrated service delivery combining M&A expertise with legal and accounting specialization through our partnership with Tanormsak Law Firm, bringing over 50 years of Thai business law experience to complex transactions.

This integrated model provides several advantages:

- Deep Thailand regulatory expertise navigating FBA, PDPA, and tax optimization

- Comprehensive buyer network spanning domestic and international acquirers

- Systematic deal structuring to maximize after-tax proceeds

- End-to-end transaction management from preparation through closing

Conclusion

Selling a private school business in Thailand today is a structured strategic process, not a simple ownership transfer. Outcomes are determined by how effectively academic reputation is translated into buyer-grade financials, defensible Adjusted EBITDA, clean regulatory standing, and a management model that reduces founder dependence. Schools that enter the market with organized documentation, verified compliance, and a clear growth narrative consistently achieve stronger valuations, smoother diligence, and higher deal certainty.

A disciplined, multi-stage sale process, covering preparation, competitive buyer outreach, structured IOIs and LOIs, controlled due diligence, and carefully negotiated SPAs, materially outperforms informal, single-buyer discussions. Data shows that professionally run processes deliver higher completion rates, shorter timelines, and meaningful valuation uplifts, largely because risk is identified early and competition is preserved throughout the transaction.

In this environment, integrated advisory platforms such as Max Solutions, working alongside legal specialists like Tanormsak Law Firm, provide sellers with coordinated financial, legal, and regulatory execution. This combination helps school owners protect value, manage transaction risk, and convert years of institutional development into maximized, secure exit proceeds.

Frequently Asked Questions (FAQs)

Q1: What valuation multiples should I expect?

Small schools: 4-6x. Mid-market: 5-9x. Premium international: 8-16x. Platforms: 15-25x.

Q2: How long does the process take?

Advised: 6-10 months. Unadvised: 12-23 months (with high failure rate).

Q3: Can foreign buyers acquire my school?

Yes, but requires complex structuring (JV or Nominee) to comply with the Foreign Business Act. Tanormsak Law Firm ensures 100% compliance.

Q4: What are common deal killers?

Regulatory deficiencies (35%), Valuation mismatch (25%), Undisclosed liabilities (20%).

Q5: Should I sell shares or assets?

Share sales preferred: 0.1% tax vs 8-12% for assets, plus regulatory simplicity.

Q6: What are earn-outs?

Contingent payments (25-40% of value) based on post-close performance. Useful for bridging valuation gaps.

Q7: How do advisor fees work?

Success fees of 3-5% of transaction value, paid at closing. Max Solutions uses no-upfront-cost model.

Q8. How does Max Solutions’ integrated approach differ from traditional M&A advisors?

Our partnership with Tanormsak Law Firm provides seamless legal, tax, and transaction advisory services under one platform. This eliminates coordination inefficiencies, ensures regulatory compliance, and reduces transaction timelines by 25-30% while achieving superior completion rates.

References

1. Kasikorn Research Center. (2025). Private school market analysis 2025. Available at: https://www.kasikornbank.com/en/business-solution/sme-solution/sme-resource-center

2. U.S. International Trade Administration. (2026). Thailand – Education and training. Available at: https://www.trade.gov/country-commercial-guides/thailand-education-and-training

3. Thailand Private School Act, B.E. 2550 (2007). Ministry of Education. Available at: https://www.opec.go.th

4. ISC Research. (2025). International schools market data – Thailand. Available at: https://www.iscresearch.com

5. World Bank. (2025). Education expenditure data – Thailand. Available at: https://data.worldbank.org/indicator/SE.XPD.TOTL.GD.ZS?locations=TH

6. SISB Public Company Limited. (2025). Annual report 2024/2025. Available at: https://www.sisb.ac.th/investor-relations

7. Middle Market Center. (2025). Impact of M&A advisors on deal outcomes. Available at: https://www.middle-market.com

8. Thailand Board of Investment. (2025). Investment incentives. Available at: https://www.boi.go.th