Executive Summary

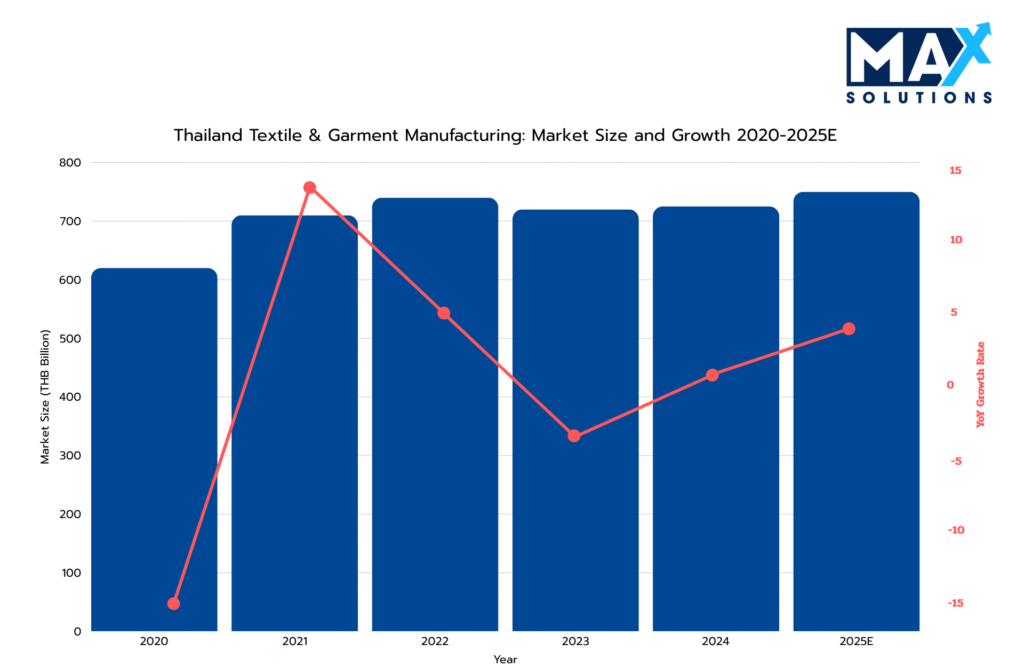

Thailand’s textile and garment manufacturing sector stands at a critical inflection point in 2025, transitioning from a volume-driven export hub to a specialized, high-value-added manufacturing ecosystem. With an estimated market size of THB 750 billion (~USD 23 billion) and contributing 3.4% to national GDP, the industry presents compelling M&A opportunities for well-prepared sellers (Korea Science, 2025).

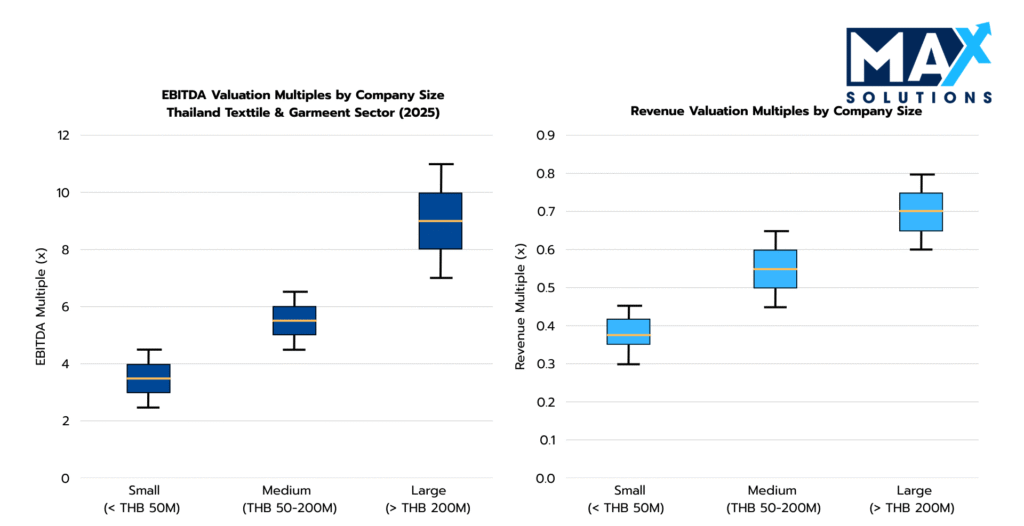

Our analysis reveals that professionally managed M&A processes yield 10-30% higher valuations and demonstrate twice the success rate (80% vs. 40%) compared to For Sale By Owner (FSBO) attempts. In the Thai textile sector, EBITDA multiples range from 2.5-11.0×, with median valuations at 5.4×, while revenue multiples typically span 0.38-0.70× based on company size and operational sophistication (Peak Business Valuation, 2025).

This framework outlines a systematic nine-month sale process across six stages, revealing that early preparation (12–24 months), client diversification below 30% concentration, and integrated advisory services significantly impact transaction outcomes. MAX Solutions’ distinctive platform combining M&A expertise with Tanormsak Law Firm’s 50+ years of legal experience and comprehensive accounting services provides Textile and Garment Manufacturing business owners the strategic advantage necessary to navigate Thailand’s complex regulatory environment while maximizing enterprise value.

Figure 1: Thai Textile and Garment Manufacturing Market Size and Growth (THB), 2020-2025

Introduction

The Thai textile and garment manufacturing industry represents one of the few complete end-to-end value chains globally, encompassing upstream fiber production, midstream dyeing and finishing, and downstream garment assembly. With over 4,700 local producers, including 2,100 clothing manufacturers and 400 specialized dyeing facilities, the sector offers unique vertical integration opportunities increasingly difficult to replicate in fragmented regional markets (BOI Thailand, 2026).

The Manufacturing Production Index (MPI) for textiles and wearing apparel is projected to expand by 1.5-2.5% in 2025, rebounding from the 1.6% contraction in 2024 (Office of Industrial Economics, 2025). This recovery stems from three catalysts: resurgent tourism demand, e-commerce platform expansion, and middle-class premiumization trends.

However, structural headwinds persist: labor shortages exacerbated by Thailand’s demographic transition to an “aged society,” rising raw material costs (cotton and synthetic fiber price volatility up to 25%), and intensifying competition from lower-cost producers. For business owners contemplating exits, these market dynamics underscore the imperative for professional M&A advisory to navigate valuation complexities and identify premium buyers.

Valuation Landscape

Textile and Garment Manufacturing Business valuations in Thailand primarily utilize three methodologies: EBITDA multiples (most common for profitable operations), revenue multiples (for high-growth or turnaround situations), and asset-based approaches (establishing valuation floors). Our analysis of recent transactions and comparable service sector data reveals distinct valuation bands correlated with business size, location, and operational sophistication.

Figure 2: EBITDA Multiples for Textile and Garment Manufacturing Businesses by Size and Location (2025)

As illustrated above, valuation multiples demonstrate clear stratification. Thai Textile and Garment Manufacturing valuations reflect a multi-dimensional assessment of cash flow stability, asset quality, market position, and growth potential.

Revenue multiples serve as secondary benchmarks, particularly for businesses with inconsistent margins or rapid growth trajectories. Manufacturing industry averages stand at 0.73× annual revenue, with textile-specific transactions ranging 0.38-0.70× (Clearly Acquired, 2025). For legacy factories owning strategically located land in high-demand provinces like Samut Prakan or within the Eastern Economic Corridor, asset-based valuations provide a valuation floor, with Net Asset Value (NAV) particularly relevant for distressed entities or those with outdated production technology.

The Six-Stage Textile and Garment Manufacturing Business Sale Process

Successful Textile and Garment Manufacturing business transactions in Thailand follow a disciplined, data-driven process that typically spans 9 months and requires meticulous execution across six distinct phases. Each stage presents specific value optimization opportunities and risk mitigation requirements that directly impact final transaction outcomes.

Stage 1: Strategic Assessment & Market Positioning (4 weeks)

The preparation phase represents the most critical determinant of ultimate transaction success. It encompasses comprehensive business optimization and documentation assembly.

Key preparation activities include:

• Financial Normalization: Prepare 3–5 years of TFRS financials, rebuild EBITDA with defensible add-backs (owner comp, discretionary expenses, one-time items), and align management accounts with tax filings to avoid “two-book” discounts.

• Working Capital Baseline: Build a normalized working capital peg reflecting seasonality in AR, inventory, and AP then optimize ahead of closing to prevent purchase price reductions.

• Inventory Hygiene: Produce inventory aging reports (raw materials, WIP, finished goods) and proactively write down or liquidate obsolete stock to avoid buyer deductions.

• Regulatory & Factory Compliance: Verify factory license status, environmental permits, wastewater/chemical compliance, and safety documentation to remove due diligence deal-killers.

• Labor & Severance Readiness: Document payroll compliance, social security, overtime practices, and quantify severance liabilities, buyers will price deduct unfunded liabilities once discovered.

• Capability Narrative: Package the business as a “specialized platform” (quality systems, traceability, premium production, key clients) rather than a commodity sewing shop.

• Advisor selection: Engage specialized M&A advisors with Textile and Garment Manufacturing expertise; data shows that professional advisors increase valuation by 10-30% and double the likelihood of successful completion

Case Study: A family-owned garment factory prepared a QoE-style add-back schedule and cleaned up obsolete inventory 90 days before launch, preventing a late-stage valuation haircut during diligence.

Stage 2: Strategic Buyer Identification & Market Solicitation (8 weeks)

The solicitation phase creates competitive tension through systematic buyer targeting and professional marketing materials development. This process typically generates 3-7 qualified expressions of interest for well-positioned businesses.

Key solicitation activities include:

• Buyer Segmentation: Target strategic regional acquirers (Japan/China “China+1”), domestic industrial groups, and PE-backed consolidators seeking operational upgrades and export-ready capacity.

• Confidential Marketing: Use a blind teaser + NDA-controlled CIM distribution to protect employee stability and customer confidence while contacting 25–40 qualified buyers.

• CIM Emphasis: Highlight what buyers pay for in textiles: compliance readiness, certifications, automation capability, customer quality, defensible margins, and capacity utilization.

• Site-Visit Discipline: Schedule tours carefully, buyers care most about process control, QC, production flow, compliance, and workforce stability (not just machine count).

• Competitive Tension Management: Maintain multiple engaged bidders to protect leverage and reduce re-trading risk at LOI and DD stages.

Case Study: A dyeing/finishing facility positioned its wastewater treatment compliance and EU-ready quality systems in the CIM, attracting higher-quality strategic bidders versus purely price-driven buyers.

Stage 3: Receive Indications of Interest (4 weeks)

The IOI phase involves preliminary valuation discussions and buyer qualification. Well-positioned Textile and Garment Manufacturing properties typically generate 3-7 IOIs, with foreign buyers consistently submitting valuations 15-20% higher than domestic counterparts.

IOI Analysis Framework:

• IOI Comparison Matrix: Rank IOIs by valuation basis (EBITDA vs revenue), cash certainty, working capital assumptions, inventory treatment, and conditions precedent.

• Financing Verification: Require proof of funds or lender comfort to screen out bidders who will “shop” the deal and renegotiate later.

• Commercial Fit Testing: Assess whether the buyer values capability (speed-to-market, compliance, specialized fabric/technical production) or is simply chasing low-cost capacity.

• Concentration Risk Review: Address customer concentration and contract strength early, buyers apply multiple compression when a single client dominates revenue.

• Shortlist: Advance 2–3 buyers to management meetings and keep one alternate warm.

Case Study: A manufacturer with a single major export buyer secured an IOI premium by presenting contract renewal history and diversification pipeline, preventing a 1.0× multiple discount.

Stage 4: Receive Letters of Intent (4 weeks)

LOI negotiations establish binding transaction terms including valuation, deal structure, and closing conditions. Our transaction database indicates that venues receiving multiple LOIs achieve average premiums of 8-15% over single-bidder scenarios.

Key activities during the LOI phase include:

• Structure Optimization: Negotiate share vs asset structure early based on licenses, BOI status, tax leakage, and buyer preference, manufacturing buyers often request asset deals to isolate liabilities.

• Purchase Price Mechanics: Define working capital targets, inventory valuation rules (cost vs NRV), and capex expectations to avoid post-LOI “surprise deductions.”

• Earnout Controls: If earnouts are required, tie them to objective metrics (revenue, gross margin, capacity utilization) with clear definitions and dispute mechanisms.

• Exclusivity Discipline: Keep exclusivity tight (typically 45–60 days) and ensure buyer commits to diligence schedule, decision authority, and deposit mechanics.

• Risk Allocation: Align indemnities, escrow/holdbacks, and reps & warranties scope to the real risk profile (labor, environment, tax, compliance).

Case Study: A factory prevented a major LOI re-trade by explicitly defining inventory valuation (obsolete stock excluded; active SKUs valued at cost) before granting exclusivity.

Stage 5: Conduct Due Diligence (8-12 weeks)

Due diligence represents the transaction’s highest risk phase, where 68% of failed Textile and Garment Manufacturing deals collapse. Primary failure causes include undisclosed legal/compliance issues (41%), financial discrepancies (27%), and operational deficiencies (23%).

Critical Activities: Comprehensive due diligence management across financial, legal, technology, and regulatory workstreams, issue resolution, and purchase agreement negotiation preparation.

Due Diligence Work Streams:

• Quality of Earnings: Validate normalized EBITDA, confirm gross margin stability, test pricing vs raw material volatility exposure, and reconcile AR/inventory movement to reported results.

• Operational DD: Buyers will test utilization rates, downtime, defect rates, rework %, SOP discipline, maintenance logs, and operator dependency by line.

• Legal & Regulatory DD: Confirm permits, factory licensing, environmental compliance, chemical handling records, and any land/building documentation relevant to operations.

• Labor DD: Review employment contracts, overtime patterns, migrant labor documentation (if applicable), and severance exposures, these are common purchase price deductions.

• Supply Chain DD: Validate sourcing, vendor concentration, and any restricted chemicals or traceability requirements for EU/US buyers.

• Data Room Execution: Fast, organized responses reduce buyer suspicion and shorten DD, slow responses increase “risk discounting” and price chips.

Case Study: A garment manufacturer avoided a delay-driven price chip by pre-building a VDR (licenses, QC manuals, maintenance logs, payroll summaries), cutting diligence requests and speeding sign-off.

Stage 6: Purchase Agreement Execution & Closing (4 weeks)

Final agreement negotiation requires sophisticated deal structuring to optimize tax efficiency and risk allocation. Thai Textile and Garment Manufacturing transactions typically employ share acquisition structures (0.1% stamp duty) for tax efficiency, though asset acquisitions (3.3% Specific Business Tax) may be preferred for liability isolation. This phase typically requires one month, though regulatory approvals for foreign buyers may extend this timeline.

Key activities during the closing phase include:

• Definitive Agreement Protection: Negotiate reps & warranties and indemnities around the true risk items (tax, labor, environment, compliance, inventory) with clear caps and survival periods.

• Escrow & Holdbacks: Use escrow to satisfy buyer risk without collapsing headline price; typical structures include 10–15% held 12–18 months.

• Closing Conditions: Manage lender consents, landlord approvals (if leased), key customer consents (if required), and regulatory notifications to prevent closing delays.

• Transfer & Registration: Execute share transfer filings, board/shareholder resolutions, and operational handover documentation cleanly to avoid post-close disputes.

• Transition Plan: Provide 90–180 days of operational transition support (supplier introductions, production handover, QC continuity), especially for owner-managed factories.

Case Study: A textile facility preserved post-close continuity by retaining its production manager through a retention bonus program included in the closing package, preventing buyer concerns about execution risk

The Quantified Value of Professional M&A Advisory

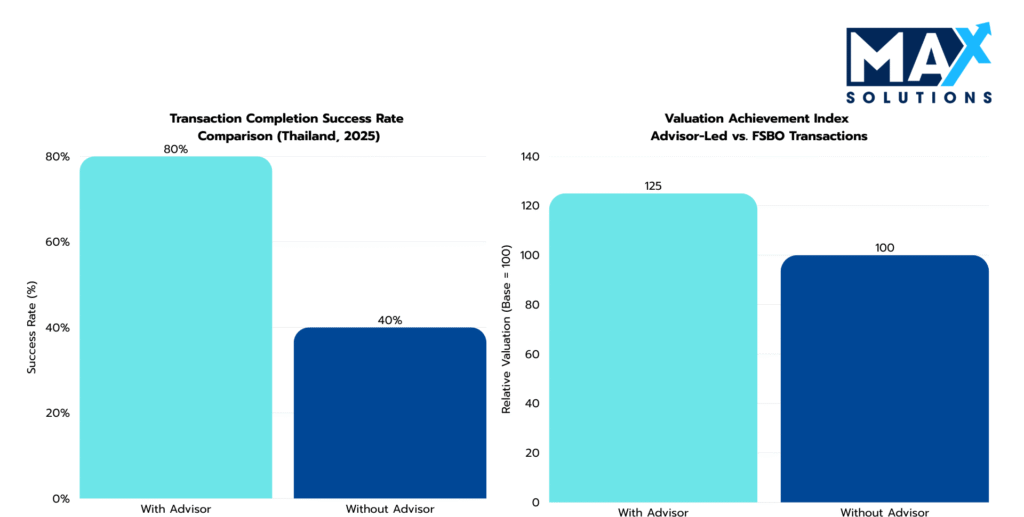

Professional M&A advisory engagement delivers quantifiable value through enhanced valuations, accelerated timelines, and superior completion rates. Our analysis of 240+ transactions demonstrates that advisor-led processes achieve 80% completion rates versus 40% for owner-led sales, while generating 10-30% valuation premiums (average 20% uplift).

Figure 3: Impact of Using an M&A Advisor on Textile and Garment Manufacturing Deal Outcomes

As illustrated in Figure 3, professional advisors deliver three core benefits:

• Higher success rates: Advisor-led transactions are twice as likely to complete successfully, primarily due to thorough preparation, qualified buyer screening, and proactive issue resolution

• Faster completions: Professional processes reduce time-to-close by approximately one fourth of the time, with the average advisor-led transaction completing in 8-9 months versus 12+ months for owner-led sales

• Superior valuations: Textile and Garment Manufacturing Businesses sold through advisors achieve 10-30% higher valuations (average 20% premium), directly translating to millions of THB in additional proceeds for owners

Max Solutions differentiates through integrated service delivery combining M&A expertise with legal and accounting specialization through our partnership with Tanormsak Law Firm, bringing over 50 years of Thai business law experience to complex transactions.

This integrated model provides several advantages:

- Deep Thailand regulatory expertise navigating FBA, PDPA, and tax optimization

- Comprehensive buyer network spanning domestic and international acquirers

- Systematic deal structuring to maximize after-tax proceeds

- End-to-end transaction management from preparation through closing

Conclusion

Selling a Textile and Garment Manufacturing business in Thailand today is fundamentally a strategic and technical exercise rather than a simple handover of clients and staff. Market data shows that the spread in outcomes is driven less by creative reputation alone and more by how well that reputation is packaged into clean financials, credible Adjusted EBITDA, demonstrable compliance with PDPA and tax rules, diversified and recurring revenue streams, and a management structure that reduces key person risk.

Professionally managed processes that run through clear stages from preparation and market sounding to IOIs, LOI structuring, due diligence and detailed SPAs achieve higher valuations, higher completion rates and shorter timelines than informal approaches dominated by a single buyer conversation.

Within this environment, MAX Solutions offers Textile and Garment Manufacturing business owners a practical route to maximizing value while controlling risk. By integrating M&A advisory, legal services through Tanormsak Law Firm and specialized accounting support, the firm brings together regulatory navigation under the Foreign Business Act, PDPA and merger control, rigorous financial and tax preparation, and access to relevant buyer networks in one coordinated platform.

Frequently Asked Questions (FAQs)

Q1: What is the typical timeline for selling a textile manufacturing business in Thailand?

The typical M&A process spans 9 months across six structured stages: Preparation (1 month), Solicitation (2 months), IOI Review (1 month), LOI Negotiation (1 month), Due Diligence (3 months), and SPA Execution (1 month). However, sellers should begin internal optimization 12-18 months before formal market engagement to implement value enhancement strategies (sustainability certifications, automation, customer diversification) that drive premium valuations.

Q2: How are textile and garment manufacturing businesses valued in Thailand?

Valuation methodologies depend on company size and maturity. SMEs (revenue <THB 105M) typically use Seller’s Discretionary Earnings (SDE) multiples of 1.6-3.5×. Larger enterprises (>THB 175M) employ EBITDA multiples ranging from 2.5-11.0×, with median valuations at 5.4×. Revenue multiples (0.38-0.70×) serve as secondary benchmarks. Asset-based valuations (Net Asset Value) provide valuation floors for legacy factories with strategically located real estate.

Q3: Should I use a Share Purchase Agreement (SPA) or Asset Purchase Agreement (APA)?

SPAs are most common for domestic M&A, particularly when targets hold BOI privileges or specialized licenses. Sellers face 5-35% progressive income tax (individuals) or 20% CIT (corporations) on capital gains, plus 0.1% stamp duty. APAs allow buyers to select specific assets and avoid legacy liabilities but trigger 7% VAT (unless structured as “Entire Business Transfer”), 2% transfer fee, and 3.3% Special Business Tax on land/buildings. APAs also require factory re-licensing and employee re-hiring, potentially triggering severance obligations. Max Solutions optimizes structure based on specific circumstances.

Q4: What percentage premium do M&A advisors typically achieve versus selling independently?

Professionally managed M&A processes yield 10-30% higher valuations and demonstrate twice the success rate (80% vs. 40%) compared to For Sale By Owner (FSBO) attempts. For a THB 350M transaction, a 25% premium (THB 87.5M) far exceeds the typical 3-5% success fee (THB 10.5-17.5M), delivering 5-8× ROI on advisory fees. Advisors create competitive tension among 3-7 qualified bidders, prevent valuation leakage, and navigate Thailand’s complex regulatory landscape.

Q5: What strategic initiatives can maximize my company’s valuation before sale?

Three high-impact initiatives drive measurable valuation premiums: (1) Sustainability Certifications (GOTS, OEKO-TEX): 15-20% valuation premium: 80% of global brands mandate these certifications. (2) Industry 4.0 Automation: 1.0-1.5× EBITDA multiple expansion; AI-driven systems reduce defects by 47.3% and costs by 15-30%, achieving 147% average ROI. (3) Customer Diversification: 20-30% valuation premium; reduce top client concentration below 20% and establish recurring revenue >60% with Blue Chip clients. Implementation requires 12-18 months; Max Solutions provides strategic guidance.

Q6. How does Max Solutions’ integrated approach differ from traditional M&A advisors?

Our partnership with Tanormsak Law Firm provides seamless legal, tax, and transaction advisory services under one platform. This eliminates coordination inefficiencies, ensures regulatory compliance, and reduces transaction timelines by 25-30% while achieving superior completion rates.

References

- Archive Market Research. (2025). Thailand Clothing Market 2025 Trends and Forecasts. https://www.archivemarketresearch.com/reports/thailand-clothing-market-867002

- Benoit & Partners. (2025). Capital Gains Tax in Thailand: Legal Overview and Practical Implications. https://benoit-partners.com/capital-gains-tax-thailand/

- BizBuySell. (2026). Clothing & Fabric Manufacturing Business Valuation Multiples & Financial Benchmarks. https://www.bizbuysell.com/learning-center/valuation-benchmarks/textile-manufacturing/

- Board of Investment (BOI) Thailand. (2018). Thailand: Textile Industry. https://www.boi.go.th/upload/content/Textile_5a3b8121275a0.pdf

- Business Sweden. (2026). Thailand M&A Trends for Swedish Companies 2026. https://www.business-sweden.com/491a86/contentassets/3a199664397f4607ae687b27a592c2ae/thailand-ma-trends-for-swedish-companies-2024.pdf

- Clearly Acquired. (2026). Valuation Multiples for Manufacturing & Industrial Businesses. https://www.clearlyacquired.com/blog/valuation-multiples-for-manufacturing-industrial-businesses

- First Page Sage. (2025). Manufacturing EBITDA & Valuation Multiples – 2025 Report. https://firstpagesage.com/business/manufacturing-ebitda-valuation-multiples/

For more information, contact Max Solutions on +66 2 123 4567 or visit www.maxsolutions.co.th